Get CREDIT CARDS and LOANS in One Click!

Get CREDIT CARDS and LOANS in

One Click!

Find top offers fast, safe, and easy!

Empowering People with Reliability and Trust

6.5M+

Users & Counting2.5M+

User Reviews5+

YearsFrom Dreams to Needs, Our Loans Bring you Instant Funds

Get the funds you need without the wait. Our loan process is quick, easy, and hassle-free—designed to give you instant access to money when you need it most.

Personal Loan EMI Calculator

Quickly Calculate EMIs for Personal, Business, Home Loans, and Loans Against Property.

All in one place. Simple, fast, and reliable.

Total Interest

Loan Amount

Loan Amount

₹5000

Total Interest

₹0

Total Amount

₹0

Your monthly EMI is

₹ 0

Tomorrow Starts with Today's Plan.

Join The Money Fair, Save spend, invest and control your entire financial life in one place.

Why Choose Us

TheMoneyFair offers secure, easy-to-use financial services with expert support and smart credit solutions designed just for you.

Easy Accessibility

Our algorithm - based technology provides easy comparism, multiple choices and unbiased advice.

Safe & Secure

Certified with ISO (27001:2013). We Built industry- best controls to keep you information secure.

Wide Choice

With over 100+ banks and NBFC's. Enjoy wide range of products and services.

Employees

With over 2000 + employees, we build an expertise service.

Customer Services

We have a dedicated and highly trained team of experts who work hard everyday to help you take best financial decisions.

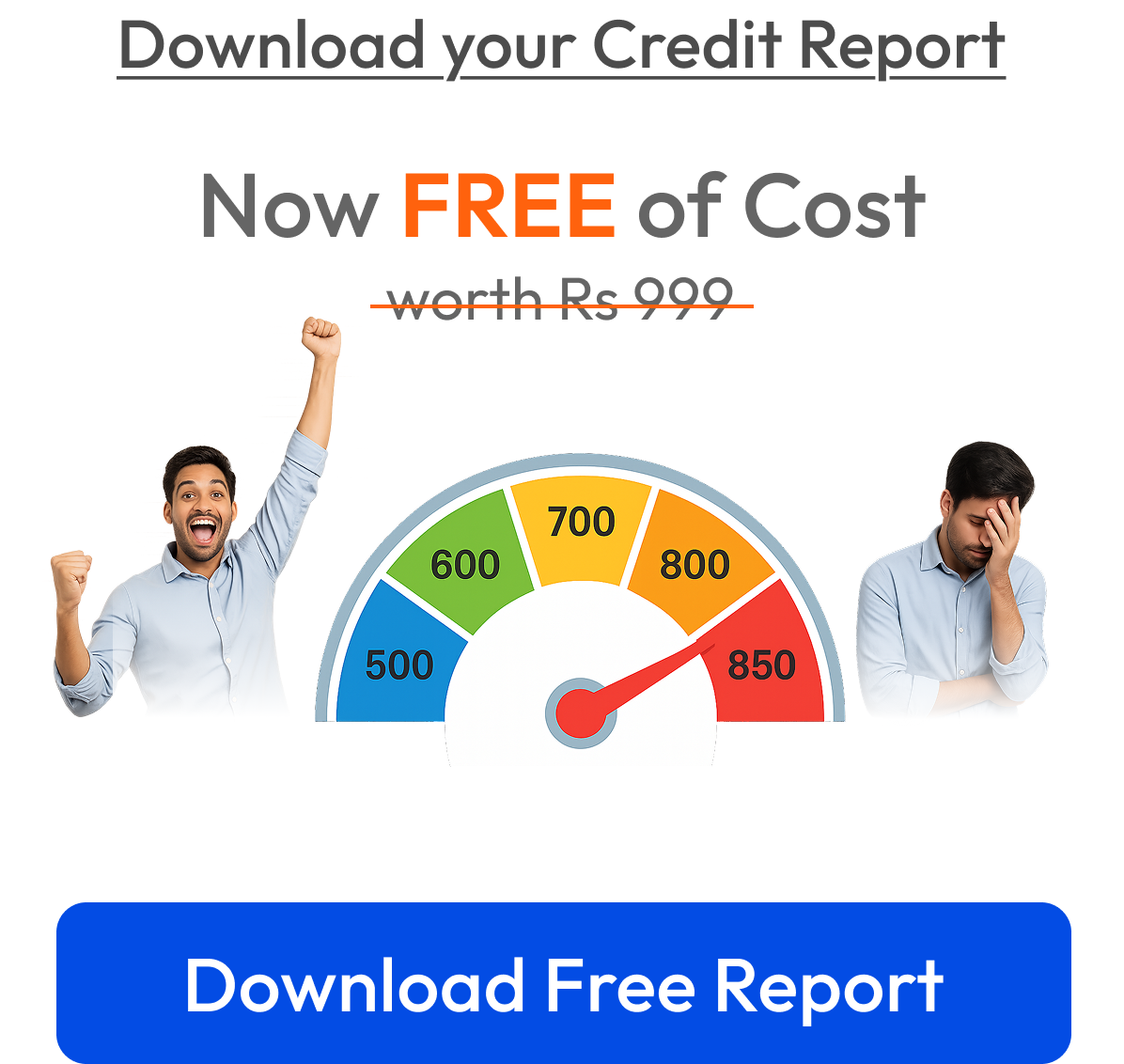

Monitor Credit Score

Stay on top of your credit score with monthly reports on credit activity, payment alerts, and insights to improve your credit score.

Increase Your Credit Potential at One Click

A credit score in the 700-749 range is considered "good" and reflects responsible credit management. Individuals in this bracket are seen as lower-risk borrowers, which opens up favorable opportunities for loans, mortgages, and credit cards.

Now or Never Deals

Limited-time offers with exceptional value. Don‘t miss the opportunity to save.

Hassle-Free Personal Loans

Enjoy a 100% paperless application process with lightning-fast approvals get the funds you need without the wait or the paperwork.

Saving Account

Open a savings account in under 3 minutes with zero paperwork seamless, secure, and entirely digital for your convenience

EMI Calculator

Easily calculate your monthly payments and plan your finances with confidence, what you’ll pay before making your next purchase.

Credit Cards

Enjoy a seamless, contactless KYC process and unlock top lifetime free credit card offers, cashback, rewards, and benefits.

Partner with Us

Join us as an advisor or partner, or pursue a fulfilling career collaborate with a team committed, growth, and success.

Our Channel Partners across Industry

Access the best deals and exclusive offers from India's most trusted banks and financial institutions—through our extensive network of channel partners.

Don‘t Take our Word for it,

See What our Clients Say

Twinkle Aggarwal

Jan 12, 2025

Excellent way to stay updated. The service is really nice —I applied for a loan and everything was done on time. Checking my credit score was super easy and quick.

Md Jawed Ansari

Feb 02, 2025

The Money Fair helped me get my Axis Bank credit card with a smooth and hassle-free process. I really appreciate the quick and efficient service. Thank you!

Saurabh Rastogi

Feb 12, 2025

Great platform to get an Axis Bank card, process was quick, easy, and completely hassle-free. Truly appreciate the fast service!